No one says you have to limit yourself to one strategy, so you can combine these and others to generate an enormous range of hybrid strategies to fit your specific financial situation. Retirement planning isn't simple.

It sounds like a lot of choices, but I think of all of these as variations of four basic strategies. The rest are either combinations of these four strategies or variations on a theme:

- Systematic withdrawal strategies

- Floor-and-upside strategies

- Time-segmentation or “bucket” strategies, and

- The “purchasing life annuities” strategy

Each strategy has a spending plan that determines how much the retiree can withdraw annually. Each strategy also has its own investment strategy, another key consideration.

Liability-matching is identifying current financial resources that will be used to pay for a future expected amount of spending. We might set aside funds now to invest to pay for college in 15 years, or identify funds that will pay for each individual year of our future retirement. A liability we may have to pay off in twenty years may be one best funded by stocks, while a liability we will need to pay in the next couple of years might be better paid with funds invested in a money market account. Some retirement strategies match liabilities with available resources and others don't.

The greatest financial risk of retirement is longevity risk, the risk that we will live so long that we run out of money. Some retirement strategies provide better guarantees against longevity risk than others.

Some strategies provide for a secure minimum “floor” of annual income that you will be able to spend no matter how the market performs. Others have no floor.

Some strategies offer the possibility of improving our initial standard of living in retirement if our equity investments perform well, while other strategies offer no such “upside potential”. And lastly, most retirement strategies leave us in control of our own retirement savings, though life annuities do not.

Let's look at the four major strategies using these eight criteria starting with systematic withdrawal strategies.

The most popular systematic withdrawal strategy is the Safe Withdrawal Rates (SWR) strategy, sometimes referred to as the “4% Rule”. It is the most commonly recommended retirement funding strategy and, since it proposes the retiree invest heavily in stocks and bonds, it is quite popular with the financial services industry. Most economists believe it is deeply flawed (I agree with them).

The amount you can spend with SWR changes depending on how much longer you expect to live in retirement and your current portfolio balance. The studies show that the annual "safe" spending rate ranges from about 4.5% of your portfolio balance the first year of retirement to nearly 10% of your remaining portfolio balance when you expect about 10 more years in retirement.

The SWR studies are often purported to show that you can spend a constant dollar amount throughout retirement that is about 4.5% of your initial portfolio value, but this is an incorrect interpretation of the study results. If you continue to spend a constant dollar amount after your portfolio decreases significantly in value, you increase the risk of depleting your savings before you die. The reverse is true if your portfolio value increases.

In practice, financial advisers will advise you to spend more when your portfolio value increases and less when it falls. Hence, the amount you can spend annually using systematic withdrawal strategies varies with major moves of the stock market, up or down.

Recently, the 4.5% “safe” rate has been revised downward to about 4% by new studies and researchers like Wade Pfau now suggest that the rate may be closer to 3.5%. A reduction from 4.5% to 3.5% may not sound like a lot at first glance, but in actuality it is a 22% decrease in the amount of money you can spend. The former provides spending of $4,500 annually from a $100,000 portfolio, compared to $3,500 a year for the latter rate.

Looked at differently, if you can safely spend 4.5% of your initial savings annually and want to spend $10,000 a year in retirement, you would need to save $222,222. If you can only spend 3.5% in retirement, you need to save $285,714. You would have to save 29% more. That 1% in question is actually a huge difference.

Even these low spending rates result in a predicted 5% to 10% portfolio failure rate. The longevity risk mitigation mechanism for these strategies is to trust back-testing that shows had you lived in 90% to 95% of rolling 30-years periods of stock market history you wouldn't have gone broke.

The spending plan for systematic withdrawal strategies is to spend an unpredictable (market-determined) 3.5% to 4.5% of current portfolio value annually with a 5% to 10% chance of going broke in old age. Reducing the spending rate improves portfolio survival chances.

Note that this spending plan is also used, at least in part, by some of the other three retirement strategies.

The investment strategy for systematic withdrawal strategies is sometimes referred to as a “total return strategy”. Rather than allocate portions of the portfolio to match various future liabilities, the strategy attempts to create a single pool of wealth, typically using modern portfolio theory's mean-variance optimization. In other words, it seeks a portfolio stock/bond allocation on the efficient frontier appropriate for the retiree's attitudes toward risk, hoping to achieve the highest possible portfolio return available for a given amount of portfolio volatility (risk).

To oversimplify, the systematic withdrawal strategies assume that if you can create a large enough single pile of capital, your other financial problems — longevity risk, a spending floor, liability matching — will take care of themselves. Systematic withdrawal strategies map all future liabilities to a single portfolio.

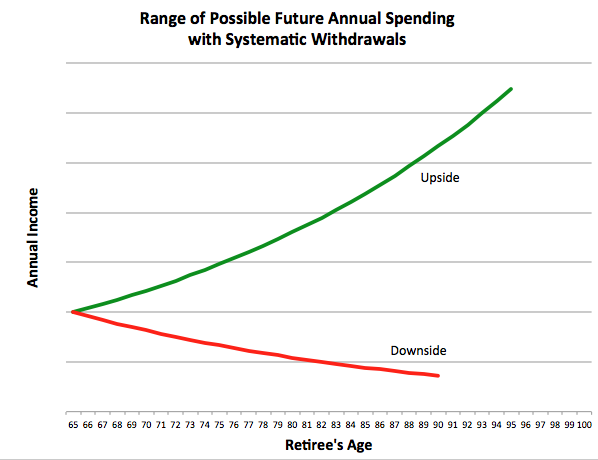

You always maintain control of your investment capital with systematic withdrawal strategies and there is a possibility that your investment results will be so good that you will be able to increase your standard of living in the future. Along with that comes the possibility that your investments will perform poorly and that your future standard of living will decline.

So, to sum up systematic withdrawal strategies, invest all your savings in a portfolio of stocks and bonds with an asset allocation based on how much volatility you can stand. Forty or fifty percent stocks would be about right for many people.

Spend 4.5% of the remaining portfolio value each year, which is an unpredictable dollar amount. (Maybe it's only 3.5%, though.) Increase the percentage gradually to about 10% when you're 85 or 90, though your portfolio balance will likely be declining as the withdrawal percentage increases.

Your future standard of living might improve or worsen, depending on your investment results. People who sell stocks and bonds will love you and you will always have control of whatever's left of your savings.

Who would be attracted to a pure systematic withdrawal strategy?

Someone who is comfortable with a 5% to 10% chance of running out of money in retirement. Someone who believes the stock market will always go back up if we wait long enough and who isn't panicked by large swings in his net worth. And someone who doesn't need guaranteed consistent annual income or a floor beneath which her spending will not drop. Perhaps someone whose income floor is adequately provide by Social Security retirement benefits and other pensions.

Some people like a dividend strategy. They buy stocks that yield high dividends and plan to spend only those dividends. They hope their stock prices will preserve their principal.

This is a variation of the systematic withdrawal strategy theme with no bond allocation and not much equity diversification, either. Due to this lack of diversification, it is riskier than the run-of-the-mill systematic withdrawal strategy but otherwise shares the same characteristics.

I'll talk about the life annuities strategy in my next post.

Good article. Looking fwd to discussion of other WD strategies, especially combo strategies.

ReplyDelete